Should You Buy Microsoft Stock After Its 25% Correction, or Run for the Hills?

Microsoft (MSFT 0.43%) It is one among a handful of hyperscalers that supply an astronomical quantity of cloud computing capability by lots of of centralized knowledge facilities scattered throughout the world. Microsoft rents this capability to enterprise clients through its Azure cloud platform, and lots of of them use it to develop and deploy synthetic intelligence (AI) software program.

Azure is persistently the fastest-growing piece of Microsoft’s total enterprise. However, traders are additionally specializing in the firm’s AI digital assistant Copilot, which is now embedded into flagship software program merchandise like Windows, Bing, and 365 (which incorporates Word, Excel, and Outlook). It represents an enormous monetary alternative for Microsoft, however adoption has been modest thus far, which has contributed to the current sell-off in its inventory worth.

Microsoft inventory is at present down 25% from its all-time excessive, however it’s now the most cost-effective it has been in additional than three years. Should traders purchase the dip, or is there extra draw back forward?

Image supply: Getty Images.

Are companies shutting down Copilot?

Copilot can be utilized as a daily chatbothowever it’s additionally a strong productiveness instrument when packaged with enterprise software program. Therefore, whereas anybody can use it for free by the Windows working system or Bing search engine, Microsoft fees a charge if companies need to embed it in the 365 software suite.

Companies at present pay for over 400 million 365 licenses for their workers (globally), so Microsoft has an enormous addressable market for Copilot. But as of the tech large’s current fiscal 2026 second quarter (ended Dec. 31), companies had solely bought 15 million Copilot licenses for 365, implying a really modest penetration price of simply 3.7%.

On a optimistic notice, that quantity grew by 160% yr over yr. Plus, the variety of companies with over 35,000 Copilot for 365 licenses tripled throughout the quarter, and day by day energetic customers soared tenfold. This means that eleven companies undertake Copilot, they have an inclination to introduce it to extra of their workers over time and dramatically ramp up their utilization.

Therefore, though some traders may be disillusioned with the modest penetration price for Copilot for 365 (therefore the decline in Microsoft inventory over the previous few months), adoption charges appear to be trending in the proper path.

Azure’s blistering development comes at an enormous value

Most AI growth occurs inside hundreds of knowledge facilities, which home of specialised chips provided by firms like Nvidia. This infrastructure prices billions of {dollars} to construct, which is why most builders lease computing capability from cloud suppliers like Microsoft Azure as a substitute.

Today’s Change

(-0.43%) $-1.75

Current Price

$408.93

Key Data Points

Market Cap

$3.0T

Day’s Range

$408.53 – $413.05

52wk Range

$344.79 – $555.45

Volume

1.8M

Avg Vol

33M

Gross Margin

68.59%

Dividend Yield

0.85%

As of Dec. 31, Microsoft had a $625 billion order backlog from clients who have been ready for extra knowledge facilities to come back on-line, which was up 110% yr over yr. That’s why the firm has invested $118 billion to construct extra infrastructure over the final 4 quarters and can spend much more going ahead.

However, there are considerations about the make-up of Microsoft’s big backlog as a result of 45% ($281 billion) is attributable to main start-up OpenAI alone. That firm solely has round $20 billion in annualized income at the second, and though it simply secured $110 billion from traders in a current capital elevate, that also will not be sufficient to meet its obligations to Microsoft — not to mention the different cloud suppliers with which it has monumental excellent commitments.

The excellent news is that Azure grew its income at a blister tempo of not less than 39% in every of the final three quarters, and administration says demand continues to exceed accessible provide. In different phrases, there seems to be greater than sufficient clients to take in any extra knowledge heart capability Microsoft brings on-line in the close to time period. The long term is extra unsure, however the firm can at all times pull again on a few of its deliberate spending if the demand setting shifts.

Microsoft inventory is beginning to seem like a cut price

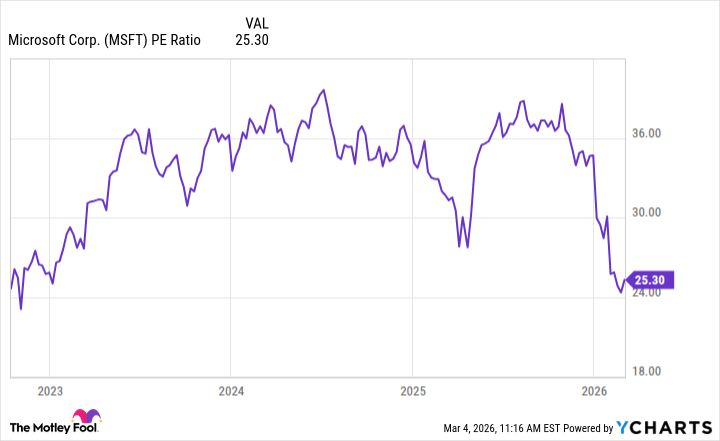

Microsoft produced earnings of $15.98 per share over the final 4 quarters, inserting its inventory at a price-to-earnings (P/E) ratio of 25.3. That is the most cost-effective stage in over three years.

MSFT PE Ratio knowledge by YCharts

Microsoft is now buying and selling at a steep low cost to the Nasdaq-100which has a P/E ratio of 31.8, so it seems very undervalued relative to a basket of its big-tech friends. The inventory can be inching towards a market a number of, since the S&P 500 (^GSPC 1.33%) at present trades at a P/E ratio of 24.7. Personally, I do not assume that is smart, given Microsoft is one among the highest-quality firms America has ever produced, which is why it typically trades at a premium to the remainder of the market.

Opportunities to buy Microsoft at such a beautiful worth do not occur fairly often, so it could possibly be an incredible addition to any long-term inventory portfolio.